Cash flow is king in an income hungry era

Financial markets are experiencing a backdrop that features low volatility and a high demand for yield. On the economic front, there are signs of stability in global growth with gradually improving credit conditions. From an investment perspective, we favor a balanced portfolio of fixed income and equity instruments that offers steady and growing cash flow. Moreover, we favor late-cycle and secular growth exposures e.g. in global industrials, energy and healthcare. Clearly, as risk assets have enjoyed a strong start to the year, we seek to be opportunistic in shaping our portfolios in a manner that offers us a margin of safety from a valuation point of view.

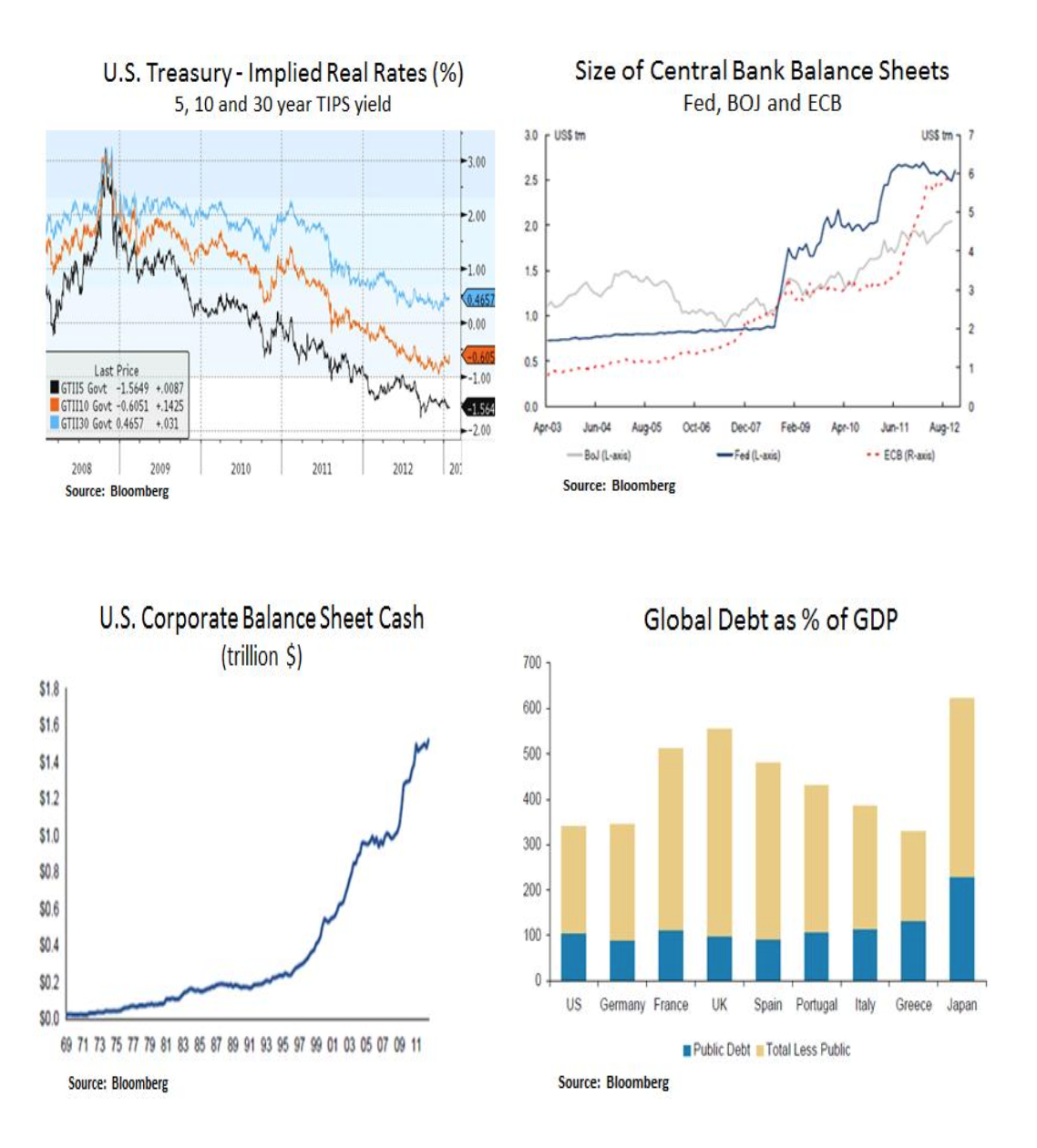

Realistically, the global central banking system is likely to continue to implement ‘financial repression’ and reflationary policies in an attempt to counter the deflationary forces of debt deleveraging. As fixed income yields become scarcer we see healthy yield and total return opportunities in MBS and large-cap dividend equities. The U.S. corporate sector has been mending its balance sheet and in a negative real rate environment CEOs are likely to continue rewarding investors with growing dividend streams and share buybacks. Sectors such as technology, industrials and healthcare in particular are cash heavy with relatively low payout ratios. Thus, we see capacity for incremental capital allocations.

From an inflation perspective, despite ample central bank liquidity, we believe excess capacity in capital and labor across the globe is likely to keep inflationary risks in check. Unfortunately, world unemployment continues to stay elevated and developed market economies in particular are still experiencing large output gaps. Subdued labor costs are likely to keep supporting corporate profit margins. Moreover, as U.S. multinationals are expanding in lower tax regimes, we see potential for further reduction in effective tax rates. Barring a recessionary environment, we see scope for steady profit margins and growing free cash flow yields. Thus, we like global multinationals with late-cycle and secular growth exposure e.g. commercial aerospace, software and emerging market healthcare spending.

At this stage of the business and profit cycle, the pace of global growth will be critical for further performance in risk assets. The latest economic data indicate signs of growth stability in China and Asian exports. In addition, as credit conditions in Europe gradually improve it is likely that some pent-up demand will be released.

Even though European corporate bond yields are very low, we believe more can be done by the ECB with regards to ensuring the competitiveness of the Eurozone; which has a higher operating leverage to global growth and emerging market growth. As global currency skirmishes are on the rise, the recent run-up in the Euro is a risk to the weaker Eurozone economies. As we can see below, there are still significant challenges for peripheral countries as they try to become competitive by devaluing internally. Moreover, the flow of capital to the private sector is still lackluster and non-performing loans are on the rise; especially in Spain as local housing market prices are declining. Therefore, more has to be done with regards to the flow of private capital and banking recapitalizations.

On the U.S. front, the housing market continues its steady recovery especially as the inventory of existing homes for sale is on the decline. Homebuilder sentiment and housing permit trends are supportive of improving housing fundamentals.

With regards to U.S. employment, new jobless claims data are supportive of a healing labor market. On the one hand we see U.S. growth benefiting from a recovering housing market and traction in the U.S. energy sector. On the other hand, we see fiscal pressures posing headwinds to consumer spending due to rising taxes. Hence, we monitor consumer and small business sentiment indicators. As such, we favor investment themes geared to corporate and emerging market consumer spending.

In conclusion, we remain opportunistic and selective in positioning our portfolios. Demand for yield is likely to remain strong in a financial repression environment. Our balanced portfolios are well positioned to generate income and healthy total returns.

Christos Charalambous CFA

Senior Strategist

christos.charalambous@edgewealth.com

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.