A View on the Information Technology Sector

Information technology investors are witnessing the convergence between the real and digital worlds. This convergence is being facilitated by increases in computing power, big data analytics and increased connectivity enabled by wireless utilization of the internet and mobile computing. According to IDC, worldwide IT spending is projected to grow 6.9% year over year to $1.8 trillion in 2012 and as much as 20% of this total spending will be driven by technologies that are shaping the IT industry e.g. smartphones, tablets, cloud computing and social networks.

From a global demographic and income class perspective, emerging markets offer the biggest opportunities as income growth will further facilitate the penetration of e.g. smartphones and IT systems to support the consequent explosion in data. As we can see below, even in developed economies there is room for growth as internet use is still not as widespread.

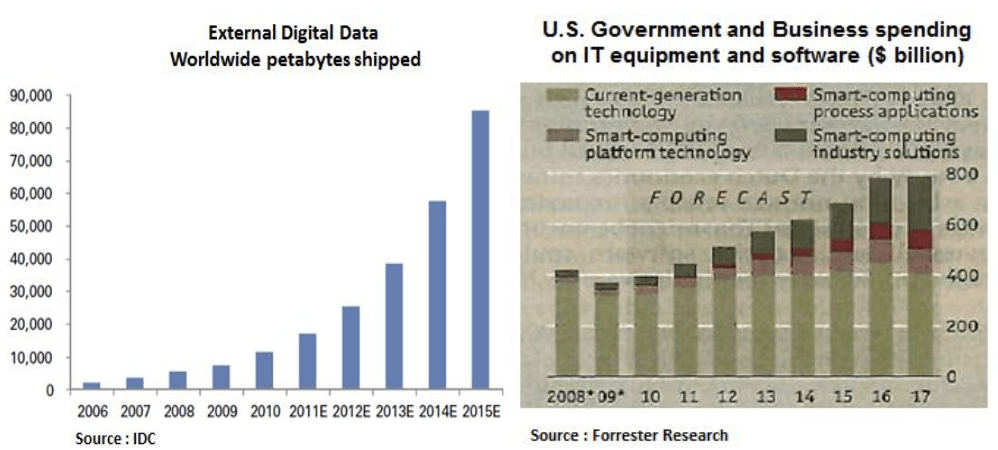

Increased volumes of structured and complex unstructured data (90% of data - e.g. text, web pages, twits, e-mail) need networks of physical and virtual servers to store and manage data efficiently. The big shift from mainframe computers to distributive computing (desktops) and now mobile computing has created a need for ‘cloud computing’ which enables data to be stored and analysed remotely via online software applications. In addition, cloud computing facilitates the seamless move of data between an ecosystem of devices. Facebook for instance is building its own servers and companies like Intel benefit from increasing chip demand from servers that store and handle these data warehouses.

Moreover, apart from retail and consumer products, big sections of the economy are driving demand for big data storage and sensor driven decision analytics e.g. financial services, energy & utilities, media & telecoms and healthcare. Thus, the convergence of the real and digital words is bringing consumers and businesses to the ‘smart age’ or ‘internet of things’ where more data becomes actionable intelligence and leads to economic growth and cost efficiencies (e.g. smart water and power grids).

In the hardware space, popularity of media/commerce centric tablet computers will likely delay PC refresh among consumers. Over time though, we recognize that as PCs have become commoditized with declining prices the household budget can afford an ecosystem of products. In addition, emerging markets are likely to support demand for PCs. On the corporate front, given the aging life of the corporate PC installed base and the strong balance sheet position of U.S. corporations, we expect the corporate refresh cycle to continue. In addition, we expect corporations to spend on areas to reduce costs and increase productivity e.g. business analytics and outsourcing of data to the ‘cloud’ in order to pay upon use. The cloud computing market is estimated to grow from $68bn in 2010 to $150bn in 2014. As such we expect cloud centric customers to become a key source in server unit growth. Industry standard server vendors are also likely to expand their ‘beyond-the-box’ services and software in order to fend off margin pressures due to commoditization.

In the software space, the big opportunity for developers arises from the demand for smartphone/tablet applications (apps). In addition, as mentioned earlier, demand for business analytics (especially for unstructured data) is likely to remain high, in order for businesses to become more efficient in turning data mining into decision making.

In the search and online advertising arena, it will be interesting to see how Google defends its market share in online advertising and how Facebook in particular will manage to monetize more effectively its 800m user base. In the search space, it will be fascinating to see how Apple’s Siri (A.I.) personal assistant may disrupt the way search is conducted on mobile computing devices. On the advertising front, another area of interest is how technology players can take aim at TV’s large share of advertising revenue.

In conclusion, although the IT sector is not immune from any medium-term cyclical risks, we like the strong secular tailwinds that the sector enjoys and we value the sector’s balance sheet capacity to grow dividends materially over time.

Christos Charalambous CFA

Senior Strategist

christos.charalambous@edgewealth.com

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.