A Delicate Balancing Act of Cyclical Momentum and Structural Hurdles

Risk assets such as U.S. equities have had a strong start in 2012 as a result of risk premium reduction in Europe and an upturn in U.S. manufacturing and U.S. labor market leading indicators. In addition, the expectation is that global central banks will continue to cushion global growth concerns by further easing their policy stance as inflationary pressures subside. Thus, we believe market confidence is supported to a large degree by policy execution, which is needed to alleviate mainly credit and structural impediments in the developed economies.

As we can see below, the ECRI leading economic indicator has continued to show signs of recovery. It is likely that the Chinese Leading Index may recover too, as European export fears ease on the back of further ECB credit accommodation by the end of this month. Thus, global manufacturing may have further legs. The U.S. equity market has kept good pace with broad economic orders and as the Fed’s Operation Twist ends in June we may see an uptick to the 10 Year Treasury yield. Growth and inflation expectations aside, the direction of the U.S. 10 Year yield will depend on the U.S. fiscal path and further risk premium reduction in Europe. Lastly, on the employment front, the downtrend in U.S. weekly claims has been encouraging for income growth and discretionary spending expectations. The latter may benefit in the medium-term by a full year extension of payroll tax cuts and unemployment benefits, which expire by the end of the month.

Apart from policy action and jobs, we believe a slow but steady recovery in housing will benefit consumer confidence by stabilizing household net worth. A steady labor market, low mortgage rates and a declining housing inventory can be another leg of support for the economy and the broader financial system. As access to credit improves, we expect house prices to gradually revert to their long-term relationship to household incomes.

To be sure, with elevated investor sentiment, this is not a time for complacency. In Europe, the ECB’s liquidity measures have managed to ease systemic risks and sovereign borrowing costs but as we can see below fundamental imbalances will take time and effective reforms in order to be rectified. Apart from credit creation risk due to banking deleveraging, Europe needs to address current account imbalances and thus enhance each country’s competitive advantage. For example, export driven economies such as Germany and the Netherlands have positive current account balances and low budget deficits and debt/GDP levels. Apart from a strong export base, the aforementioned countries derive their competitive advantage from low labor costs. Therefore, given the complex and fragmented politics of Europe, one should expect further volatility until these economic divergences within Europe get corrected.

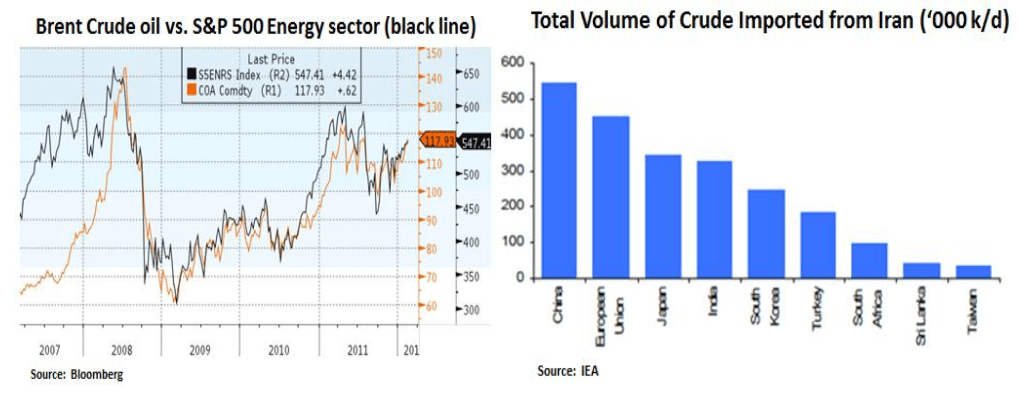

Geopolitical risks in the Middle East and their impact on crude oil are another wildcard for financial markets. European imports of Iranian oil may not be easy to replace. In addition, with Brent already at $118, a further and sustained increase in crude oil will be a hindrance for energy intensive emerging markets. A high oil price (>$125) can cause global growth to slow and may thus destroy oil demand in the process. Ironically, this may hurt the energy sector if geopolitical risks get out of hand.

Lastly, with a projected ~3% fiscal drag to GDP in 2013, markets and CEOs may lose confidence if U.S. decision makers don’t provide a credible fiscal plan that will address overall government indebtedness and entitlement spending, which is progressively becoming a larger portion of the federal budget as baby boomers start retiring. Declining labor participation and thus a contracting tax base need to be addressed.

In conclusion, we continue evaluating the market’s risk-reward profile and we maintain a balanced portfolio of income generating instruments and selective undervalued securities.

Christos Charalambous CFA

Senior Strategist

christos.charalambous@edgewealth.com

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.