U.S. housing, jobs recovery and energy renaissance are key levers for growth

Perceptions of household net worth and permanent income generation are important pillars in every economy. Stability in the housing and jobs markets are key ingredients for the ongoing U.S. economic recovery, as more than 70% of U.S. GDP is generated by consumer spending. In addition, the above components bode well for the proper functioning of the U.S. credit system.

As we can see below, the gradual recovery in the jobs market has been an important support for risk assets since 2009. The pace of firings has been steadily declining and businesses have been opening more job opportunities. The unemployment rate has been declining more slowly due to structural imbalances e.g. as a consequence of excess supply of labor in the housing and financial sectors. Over time though these imbalances will be rectified as the skills mismatch is addressed. From a cyclical perspective, a recovery in lending to businesses and a recovery in corporate profitability can lead to more sustainable job growth as companies plough back profits in the economy and engage in capital and labor expenditures in order to grow. As of late, non-farm productivity growth has been slowing as corporations have taken full advantage of producing output with less labor. At this stage in the cycle, companies need to hire in order to meet customer demand. In addition, they need to spend more in business equipment in order to achieve better productivity growth. Therefore, given the healthy state of corporate balance sheets, we believe job growth can be sustained. A key catalyst or risk to the pace of job growth will be policy execution with regards to the U.S. fiscal path, as we discussed in past articles.

The U.S. banking system is now creating credit again for small businesses and consumers. Increasing credit availability to small and medium sized businesses has been a key component in the economic recovery. Small businesses account for ~50% of hiring in the U.S and as we can see below growing business optimism has been a contributing factor to small business hiring plans. A key issue for small businesses has been lack of sales and as the economy recovers, temporary workers should be converted to permanent hires. In addition, more clarity on future healthcare costs may act as a further catalyst to small business confidence and thus hiring.

For small business owners, stability in the housing market is very important as housing constitutes a large component of their net worth. In addition, the cost and ability to service their financial obligations is a key driver of small business confidence. As we can see below, a combination of debt restructuring and low interest rates has given consumers more leeway in their spending budgets.

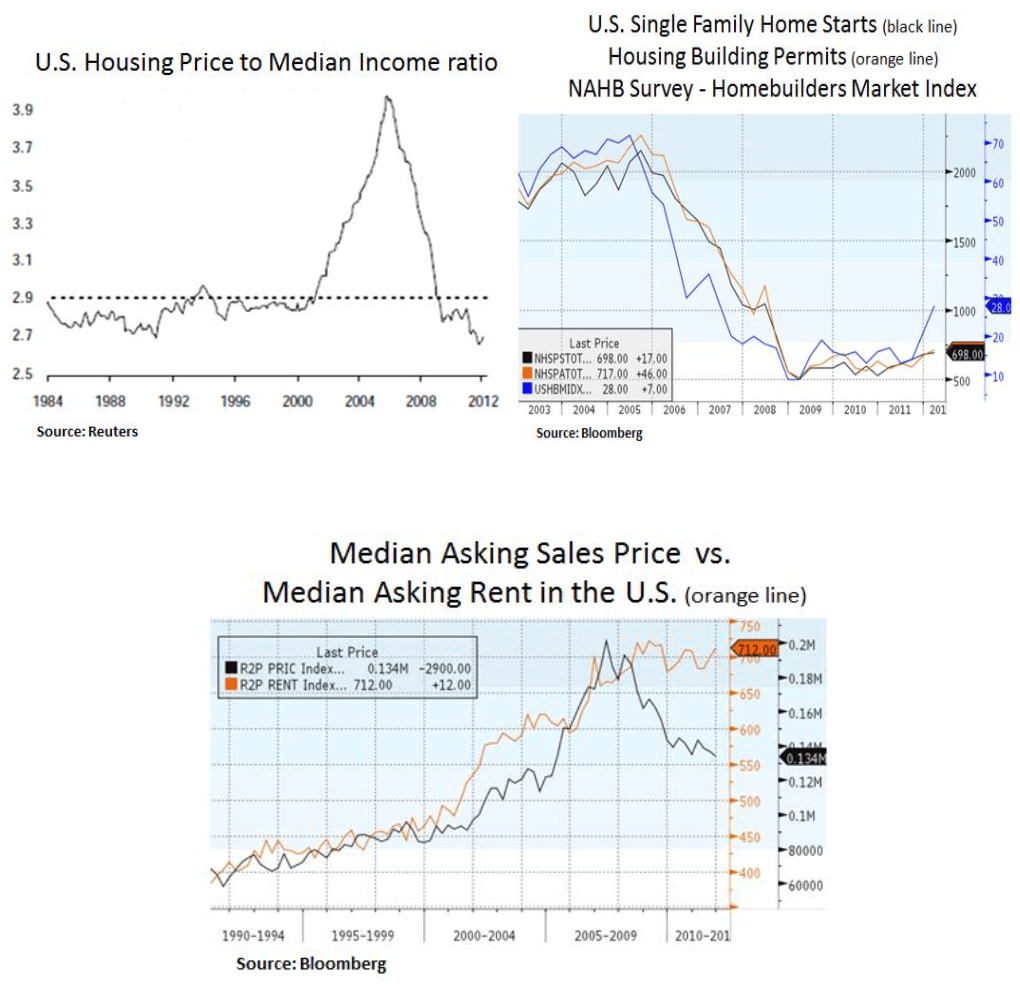

We believe the housing market is in a bottoming process. Increasing affordability and credit availability have contributed to a slow but steady recovery in housing starts and building permits. We expect the foreclosure pipeline to ease gradually over the next 4-5 years as excess supply is chipped away by household formation. As we can see below, elevated rent costs are likely to spur demand for home ownership. Therefore, stability in housing can help stability in the credit and jobs markets as well, reinforcing perceptions of household wealth and permanent income generation.

As we discussed in past articles, fiscal and entitlement spending visibility is needed in order to inspire confidence in businesses and consumers alike. For example, excess healthcare costs need to be addressed. Fiscal and entitlement spending instability may weigh on sentiment by year-end, and thus a policy mistake is a risk.

On a more positive note, despite the aforementioned structural impediments, we need to highlight the material structural shift in the energy sector. As we discussed in our energy sector reports (please see appendix), the U.S. energy sector is enjoying an energy resource renaissance as a result of oil and natural gas drilling in shale formations. The outlook for oil and natural gas production is very promising and if proper policies are put in place, growth in the energy sector may help alleviate the nation’s energy bill and current account deficit. As we can see above, drilling in oil fields has been unabated. On the natural gas side, in the short-term there has been excess supply but over time we expect demand for natural gas to increase as power generators use it as a preferred fuel and as natural gas becomes a surface fuel e.g. for trucks. Therefore, the energy sector can help the ongoing economic and jobs recovery and also contribute to the gradual reduction of the budget deficit.

To be sure, we live in an interconnected global economy and as we discussed in last week’s article, further policy responses in Europe and China can help stabilize the global growth outlook. On the European front in particular, it has been encouraging that the ECB’s renewed presence as a lender of last resort has led to a decline in sovereign yields and in the risk premium in the corporate and financial debt markets. Lending trends in U.S. and Europe have been diverging and future stability in European lending trends is important, especially in the face of ongoing banking deleveraging. Yet, support from the ECB can help at least in keeping refinancing costs low.

In conclusion, we highlight the ongoing recovery in the ECRI leading economic indicator. The U.S. growth outlook is likely to be on a moderate trajectory for the rest of the year and as we discussed above we expect the gradual recovery in the housing and labor markets to be important milestones for the continuation of this business cycle. From a portfolio perspective, we continue to seek yield and value opportunities in instruments that offer cash flow visibility and stable returns on investment.

Appendix:

http://www.edgewealth.com/updates/archive/2011/a-view-on-us-oil-industry-dynamics/

http://www.edgewealth.com/updates/archive/2011/n-american-energy-infrastructure-view/

http://www.edgewealth.com/updates/archive/2011/a-view-on-us-power-generation-prospects/

Christos Charalambous CFA

Senior Strategist

christos.charalambous@edgewealth.com

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.